Asset allocation is the relative percentage of stocks and bonds in your portfolio. Over time, it determines your investment results.

The takeaway: Asset allocation, the percentage of stocks and bonds in your portfolio, is the main driver of how fast your nest-egg grows. It’s a tool that, when followed, forces you to buy low and sell high. Master this principle and make sure you’re prepared for the next recession.

$$$

Boomer, early in the year is the perfect time to discuss the topic of asset allocation. Here’s what asset allocation does for you:

- it supercharges your investment returns and

- it provides the framework for buying low and selling high.

What’s not to love?

But here’s the thing. You can’t reach this holy grail of investing until you meet the prerequisite. Once you meet the prerequisite, you won’t panic with every gyration of the market.

The relative percentage of stocks and bonds in your portfolio determines your investment returns.

And the prerequisite is that you’ve got to be crystal clear on how and why the relative percentage of assets in your portfolio determines your investment returns.

These relative percentages are key to helping ensure that your money lasts as long as you do.

These relative percentages are called asset allocation.

What’s asset allocation?

In its simplest form, asset allocation is the percentage of stocks and bonds you have in your investment portfolio—like your IRA, 401(k), etc. To keep it simple, we’re talking about stock and bond mutual funds–preferably index funds. Index funds are a type of mutual fund and are discussed here.

To keep it simple, we’re talking about stock and bond mutual funds.“

Your investment returns are determined by the relative percentage of assets in your portfolio.

Boomer, how successfully you grow your portfolio depends on the relative percentage of assets you have in your portfolio, like stocks and bonds.

Why?

Because different assets appreciate faster than others.

A portfolio with 80% stocks will have substantially higher investment returns than a portfolio with 80% bonds.

Why? Because,as we’ll show below, stocks appreciate substantially faster than bonds.

Just how much faster do stocks appreciate than bonds?

Bonds are relatively stable and slow growing. Stocks grow relatively quicker, but are volatile.

A lot, according to data from the Federal Reserve database in St. Louis and compiled by my former UCLA finance instructor–Aswath Damodaran–currently at the NYU Stern School of Business.

Say your beloved grandma deposited $100 in the stock market back in 1927, and never invested another dime. Today, after the stock market crash of the Great Depression, the stock crash of the Great Recession, and assorted other stock market calamities, by year-end 2017, she’d have had $399,769. In contrast, if she’d bought those risk-free U.S. Treasury bonds, she’d have $7,310.

$100 invested in the stock market in 1927 would be worth $399,769 today. That same amount invested in risk-free Treasury bonds would be worth $7,310.“

Grandma’s stocks appreciated 11.53% a year, while her bonds appreciated 5.15% a year.

Stocks are where you put money you won’t need any time soon–like in the next 10 years.

Here’s the thing, Boomer. Stocks are volatile. They soar heavenward and crash to hell. But overall, and over time, stocks go up.

With stocks appreciating an average of 11.53%, your money doubles every 6¼ years on average. With bonds appreciating at 5.15

% a year, your money doubles every 14 years, on average.

What do you want: doubling your money on average every 6¼ years or every 14 years?

(Check out the glossary’s Rule of 72 to see how long it takes money to double.)

Stocks appreciate faster than bonds.

The larger the percentage of stocks in your asset allocation, the faster your portfolio appreciates.

If bonds are so inferior, why own them?

You own bonds because they balance the volatility of stocks.

Because, unlike grandma, you don’t have 90 years to endure the stock market’s ups and downs before taking big profits. Stocks are volatile, while bonds are relatively stable and consistent. Also, although it’s not a perfect one-to-one correspondence, bonds tend to rise when stocks fall. We saw this during the Great Recession.

A key to asset allocation–and investment returns–is understanding how to play the high appreciation of stocks against the plodding stability of bonds.“

Using data again from the Federal Reserve, and compiled by NYU, say you had $2,000 in savings–$1,000 in stocks and another $1,000 in Treasury bonds at year-end 2007. When the Great Recession hit in 2008, stocks plummeted 37%. However, Treasury bonds actually went up 20%. Your portfolio’s net return would have been a minus 9%.

A 9% loss is recoverable. You’d feel a lot better withdrawing living expenses from a portfolio that was down 9% vs. one that was down 37%.

This, my smart Boomer, is why you want both stocks and bonds in your asset allocation. (And remember, to keep it simple, we’re talking about buying bond mutual funds.)

In short, the key to asset allocation–and investment returns–is understanding how to play the high appreciation of stocks against the plodding stability of bonds.

Stocks crash, but like the phoenix, they rise again—and they rise big

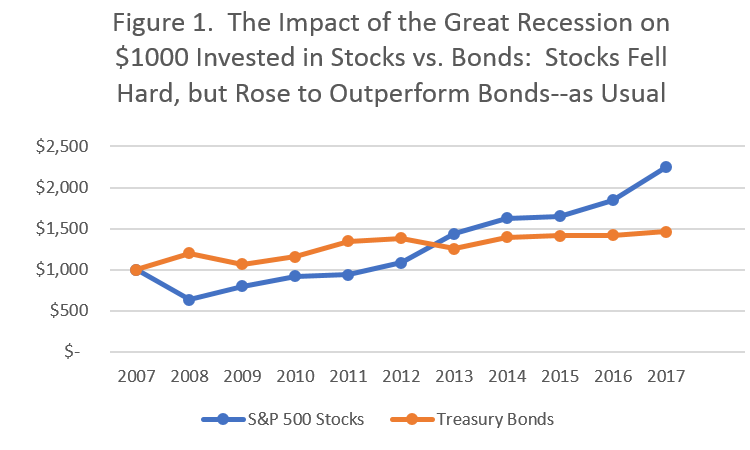

If you didn’t panic and sell during the Great Recession, and continuing with the above example, Figure 1 below shows that by 2012 your stocks would have been back up to the initial $1,000 you’d saved. By year-end 2017, that initial $1,000 stock investment would be worth $2,245. In contrast, your bond portfolio would be worth $1,460.

That, dear Boomer, is a 54% difference!!

The lesson here Boomer is that stocks are where you put money you don’t need right away. It took four years from the crash for your stocks to get back to even. However, in another four years, stocks were once again crushing bonds and your portfolio was sailing.

Stocks are volatile.

Volatility is the price of admission for investing in the market.

Your job is to properly allocate the percentage of stocks and bonds you have in your portfolio.

Up next: What percentage of stocks and bonds should you consider for your portfolio?

There are standard rules of thumb for the percentage of stocks and bonds you might consider for your portfolio.

There are rules of thumb to help you consider the relative percentages of stocks and bonds you might want in your portfolio.

You want a large enough percentage of stocks in your portfolio to ramp up your investment returns, but you always want the steady hand that bonds provide.

It’s a delicate dance, smart Boomer. We’ll discuss these rules of thumb in the next post in this series.

In the meantime, look at your portfolio. What percent do you have in stocks and what percent is in bonds?

Have a great 2018, Boomer. May you be prepared for anything the market brings. (And remember, asset allocation is key.)

$$$