If you buy a stand-alone long-term care policy, understand you’re buying from an industry in chaos. With nursing home costs approaching $100,000 annually, heed these five warnings before you buy.

The takeaway. If you buy stand-alone long-term care insurance, prepare for rate hikes, prediction failures, and the fact that you might not even need the insurance. Your mileage may vary. 😐

$$$

Boomer, before you buy stand-alone long-term care insurance, consider the case of Mary Jo Klimenko. I came across her story in Kaiser Health News (as reported by Barbara Feder Ostrov).

It nearly set my hair on fire.

Ms. Klimenko bought a long-term care policy 20 years ago. Like life insurance, the younger you are when you buy, the cheaper the policy is supposed to be. But her rates have unpredictably increased so much, she’s no longer sure she can afford the policy.

In the last two years, her rates quadrupled.

(Imagine the national outrage if car insurance quadrupled over a two-year time period.)

Now, at 69 years-young, she wishes she’d just banked all those insurance premium payments.

Her situation isn’t unique.

The industry is in chaos.”

What you should know.

Stand alone policies are the cheapest long-term care policies you can buy–and they cost plenty. Fortunately, there’s a new kid in town, called the hybrid, that is catching on. But until it does, stand-alone policies are still being written to the unsuspecting.

If you buy one, here are the five warnings you should know.

#1. Insurers are imposing massive rate hikes.

Boomer, throughout the country, insurers are substantially raising premiums.

Boomer, throughout the country, insurers are substantially raising premiums.

- The federal government raised most of its employee long-term care premiums by 83% in 2016, according to Forbes.

- Over the last two years, Chicago’s CNA Financial Corp. has raised some policyholder’s rates more than 90%, according to the Wall Street Journal.

- Genworth’s 2017 rate increase was such that the company had to set up a website just to deal with consumer fall-out.

- California raised state employee rates by 85% in 2016, according to Kaiser Health News.

- And perhaps the worst of all is the case of Pennsylvania’s Penn Treaty. While not raising its rates, per se, for nine years the company pocketed customer premiums and didn’t pay their nursing home costs, according to the New York Times. The company was apparently fighting to stay out of bankruptcy during those nine years. It failed.

And so it goes.

The industry is in chaos.

#2. You pay the price for insurers’ prediction failures.

When your rates go up, you’re generally paying for failure. Here’s how. Insurance is a game of prediction. The long-term care insurance industry predicts:

When your rates go up, you’re generally paying for failure. Here’s how. Insurance is a game of prediction. The long-term care insurance industry predicts:

- how long people will live;

- how much interest they can earn on customer premiums; and

- how much money they’ll make when customers let their policies lapse.

When the industry gets these three things right, they generate enough money to pay out claims. If they get them wrong, they raise your rates.

Suffice to say, they’ve gotten it wrong.

With rate increases in double- and triple-digit percentages, the long-term care insurance industry punishes you for their prediction failures.”

A 2016 report by the National Association of Insurance Commissioners, in conjunction with the Center for Insurance Policy and Research, (p. 19), states that customer premiums have significantly risen because:

- people are living longer than insurers anticipated;

- interest earned on customer premiums has been historically low; and

- fewer people are letting their policies lapse.

Let’s be clear, in their own veiled way, the National Association of Insurance Commissioners is acknowledging the industry’s prediction failures.

These prediction failures are passed along to you in the form of double- and triple-digit rate increases.

#3. Most insurers have abandoned selling new long-term care policies.

Between 2000 and 2016, the number of insurers writing new long-term care policies dropped by 90%. In 2000 there were 125 companies selling at least 2,500 policies a year. Today there are 12.

Between 2000 and 2016, the number of insurers writing new long-term care policies dropped by 90%. In 2000 there were 125 companies selling at least 2,500 policies a year. Today there are 12.

Those companies still selling new long-term care policies are:

- Bankers Life and Casualty

- Genworth Financial

- John Hancock Financial Services (Individual Market)

- Knights of Columbus

- LifeSecure

- MassMutual Financial Group

- MedAmerica Insurance Company

- Mutual of Omaha

- New York Life Insurance

- Northwestern Long Term Care Insurance Company

- TransAmerica Life Insurance

- Thrivent

Are you still paying on a policy that’s not listed above?

Don’t be alarmed. Your company may sell less than 2,500 policies a year. Or, it may be collecting customer premiums and honoring customer claims, even though it no longer sells new policies.

And why aren’t companies selling new policies?

Because, most commonly, they can’t make a sufficient profit, according to the National Association of Insurance Commissioners.

Failures in prediction vaporize profits.

#4. Before you buy, consider that you probably won’t be in a nursing home—at least not for long.

With rates approaching $100,000 a year, nursing home costs can be catastrophic for you and your family.

With rates approaching $100,000 a year, nursing home costs can be catastrophic for you and your family.

Most long-term care is delivered in the home.”

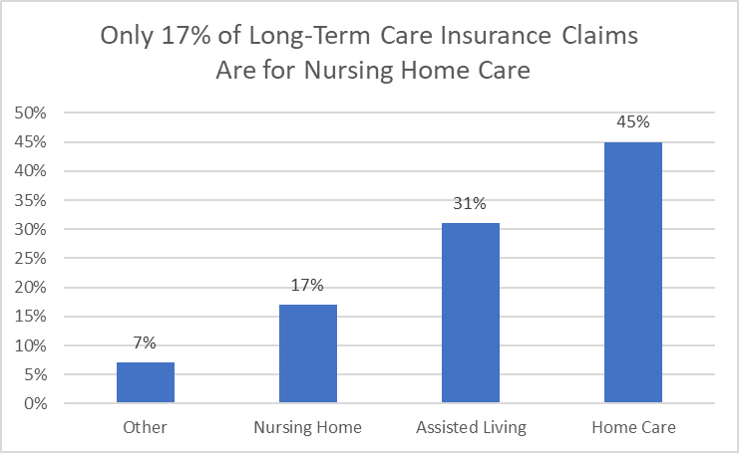

Fortunately, relatively few people receive long-term care in nursing homes—only 17%–according to researchers over at LifePlans (p.9). They reviewed a random sample of 600 claims submitted to 11 of the industry’s largest long-term care insurers.

As shown in the chart below, only 17% of long-term care claims were for nursing home care. You can see that most care is delivered in the home.

Source: “Experience and Satisfaction Levels of Long-Term Care.” LifePlans, p. 9, September 2016.

Not only is nursing home care infrequent, but stays are short. Boston College researchers indicate that 39% of men and 50% of women never have a nursing home stay exceeding three months (p 4).

They report that many of these stays are likely covered by Medicare. Medicare pays for 100 days of nursing home care if it follows three “qualified” nights in a hospital. (Check with your doctor’s insurance staff and your state’s Medicare program. And remember, Medicare does not generally pay for long-term care exceeding 100 days.)

Boomer, the point here is don’t over-insure. Long-term care provided in the home and in assisted living is less than half the cost of a nursing home.

Don’t over-insure!“

#5. Only a minority of those turning 65 will need long-term care for more than a year.

In an different post, we discussed the odds of anyone needing long-term care. We saw that on average,

In an different post, we discussed the odds of anyone needing long-term care. We saw that on average,

- a little over 50% will never need any long-term care at all and

- 19% will need it for less than a year.

That’s over two-thirds of the population who, if they need long-term care at all, will need it for less than one year! Hopefully you’ll be in that category.

So what do you do now?

Before you buy, protect yourself by taking these action steps!

- Don’t over-insure. Again, with feeling: Don’t.over.insure. If you need care at all, the research above shows it could well be for less than three months.

- Review my earlier post that showed the costs and odds of your needing long-term care. Weigh those odds!

- Protect your wallet by reading the rest of the long-term care series (listed below); read and save!

In the meantime, be wise, savvy Boomer.

You’ve got options.

$$$

P.S. Hey, there! If you think this post would help someone else, could you pass it along or post it on Facebook? Thanks! You rock!

$$$

-

Long-Term Care Series (Oldest to Newest)

- Long-Term Care Insurance: Five Warnings Before You Buy

- Long-Term Care Insurance Quiz: Will I Need It? Can I Get It?

- 17 Ways to Get Turned Down for Long-Term Care Insurance. (And What Happened to Me.) ** Most popular post on blog!

- Getting Medicaid to (Maybe) Pay for Your Nursing Home Costs: The (Updated) Epic Guide!

- Three Types of Long-Term Care Insurance: You Might Not Need Any!

- Continuing Care Retirement Communities Part 1 —Seven Essential Things to Know

- Continuing Care Retirement Communities Part 2 — Four Ways to Figure Out if They’re Worth the Money

- Continuing Care Retirement Communities, Part 3 — What to Ask Before Signing on the Dotted Line.

- Staring Down Your Long-Term Care Odds–Much Better News Than You Thought.

- How to Evaluate a Long-Term Care Policy. (Hint: Know These Three Things.)

- The Three Factors Affecting Your Long-Term Care Insurance Costs

- My Encounters in the Wild With Long-Term Care Sales Agents.

$$$